Legacy Planning: Your 100 Year Plan

Note: The following is excerpted from The Wright Exit Strategy - Wealth; How To Create It, Keep It and Use It authored by Bruce Raymond Wright. Bruce updated it slightly for this website in June 2014.

|

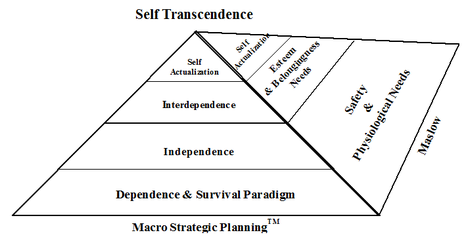

When we’re taking a look at overall planning, strategies and so forth, we have to realize that we have different needs at different times. We agree with psychological theorist Abraham Maslow who also believed that human beings have a tremendous potential for personal development and positive growth. However, there are certain needs that have to be satisfied before we can reach what he called “self-actualization,” the point at which we become the best that we can be at a particular point in our lives.

|

Maslow developed a “hierarchy of needs” triangle that demonstrates the different levels of human awareness or consciousness and needs:

|

Readers familiar with Dr. Maslow’s work will notice that I have taken some liberties with Maslow’s triangle and have expanded it into a multidimensional pyramid. This abbreviated version offers an effective visual aid that I am happy to discuss with those who want to explore the subject deeper.

The first level at the bottom of the pyramid describes human survival. You have to put food in your mouth, a roof over your head, and clothes on your body. When you’re living at this level, you tend to think, “I’ll dig ditches 12 hours a day if I just could have some food in my belly and a warm, dry place to sleep at night.” So you start to dig ditches, but then after awhile, your belly is full and you begin to become dissatisfied. You see the guy who’s in charge of the people digging ditches and you notice, “Gee, he’s got a better life than I do. I wish I could have a life more like that.” That is when you begin to elevate your desires and then awareness so you can elevate yourself beyond fundamental survival and into other more rewarding, evolved levels of working, living and enjoying life.

Maslow’s hierarchy of needs is relevant to understanding people’s level of acceptance or readiness to participate in Macro Strategic Planning® or in advanced career, wealth management or relationship management. For example, I believe that my first priority should be to provide for myself and my dependents during our lifetimes, making the most of what we have so that we are enjoying a good quality of life. But, I have taken measures to raise my children so they are equipped to succeed on their own, without my financial support. It is wise to begin longer term thinking such as, “I don’t know what our health is going to be, physically or mentally, five years from now or 50 years from now and I have an obligation to my children and society to ensure that my wife and I will not become a burden to other people.” A lot of people have become burdens to society or burdens to future generations because they have failed to secure their own financial independence. If you believe that being old, tired and impoverished isn’t what you want to experience, you must take relevant, effective and timely action to create your own financial, physical and emotional security.

The next priority tends to be an emotional, philosophical and partly a timing decision which is, “What am I going to do with the assets over and above what my wife and I need?” Personally, I still have children at home, and I believe it’s my responsibility to make sure that my children do not become a burden to anyone else or to society. So I have implemented and funded strategies and tactics which take care of my children to the extent that I want them provided for. I have created an appropriate safety net which does not include disincentives to their personal sense of growth, significance and desire to succeed in their own way, on their own terms.

With any excess assets over and above that, I believe I have a moral obligation to direct the balance of my wealth to viable causes rather than forfeit it to the State or Federal government. If you are financially successful, there’s a portion of your wealth that you cannot freely give to your children even if you want to. Uncle Sam won’t let you. Your only choices for that particular amount are: A) to give it to charity; or B) to forfeit that wealth to the government through estate taxes.

If you believe that the government is the best steward for your money, or at least 55% of your money, then don’t proactively take charge of your wealth. By not taking proactive, preemptive action now, the government will take what you thought was your wealth and spend it on all kinds of things you may disagree with. Because of your lack of appropriate and timely action or your lack of knowledge, you will choose Congress over your preferred causes by default. But you have a choice.

Capital gains and estate taxes are in fact options, not mandates for those who possess the right kind of knowledge, then take appropriate and timely action. You can choose to designate what cause(s) your wealth will support if you plan for it now and make it a part of your agenda. You can use the portion of your wealth that would have gone to Uncle Sam and put it back into your community, finance a legacy or a personal or family mission statement. You can choose to fund your grand passions, purposes and missions or you can forfeit your wealth to politicians and bureaucrats who deem themselves to be wiser than you.

The first level at the bottom of the pyramid describes human survival. You have to put food in your mouth, a roof over your head, and clothes on your body. When you’re living at this level, you tend to think, “I’ll dig ditches 12 hours a day if I just could have some food in my belly and a warm, dry place to sleep at night.” So you start to dig ditches, but then after awhile, your belly is full and you begin to become dissatisfied. You see the guy who’s in charge of the people digging ditches and you notice, “Gee, he’s got a better life than I do. I wish I could have a life more like that.” That is when you begin to elevate your desires and then awareness so you can elevate yourself beyond fundamental survival and into other more rewarding, evolved levels of working, living and enjoying life.

Maslow’s hierarchy of needs is relevant to understanding people’s level of acceptance or readiness to participate in Macro Strategic Planning® or in advanced career, wealth management or relationship management. For example, I believe that my first priority should be to provide for myself and my dependents during our lifetimes, making the most of what we have so that we are enjoying a good quality of life. But, I have taken measures to raise my children so they are equipped to succeed on their own, without my financial support. It is wise to begin longer term thinking such as, “I don’t know what our health is going to be, physically or mentally, five years from now or 50 years from now and I have an obligation to my children and society to ensure that my wife and I will not become a burden to other people.” A lot of people have become burdens to society or burdens to future generations because they have failed to secure their own financial independence. If you believe that being old, tired and impoverished isn’t what you want to experience, you must take relevant, effective and timely action to create your own financial, physical and emotional security.

The next priority tends to be an emotional, philosophical and partly a timing decision which is, “What am I going to do with the assets over and above what my wife and I need?” Personally, I still have children at home, and I believe it’s my responsibility to make sure that my children do not become a burden to anyone else or to society. So I have implemented and funded strategies and tactics which take care of my children to the extent that I want them provided for. I have created an appropriate safety net which does not include disincentives to their personal sense of growth, significance and desire to succeed in their own way, on their own terms.

With any excess assets over and above that, I believe I have a moral obligation to direct the balance of my wealth to viable causes rather than forfeit it to the State or Federal government. If you are financially successful, there’s a portion of your wealth that you cannot freely give to your children even if you want to. Uncle Sam won’t let you. Your only choices for that particular amount are: A) to give it to charity; or B) to forfeit that wealth to the government through estate taxes.

If you believe that the government is the best steward for your money, or at least 55% of your money, then don’t proactively take charge of your wealth. By not taking proactive, preemptive action now, the government will take what you thought was your wealth and spend it on all kinds of things you may disagree with. Because of your lack of appropriate and timely action or your lack of knowledge, you will choose Congress over your preferred causes by default. But you have a choice.

Capital gains and estate taxes are in fact options, not mandates for those who possess the right kind of knowledge, then take appropriate and timely action. You can choose to designate what cause(s) your wealth will support if you plan for it now and make it a part of your agenda. You can use the portion of your wealth that would have gone to Uncle Sam and put it back into your community, finance a legacy or a personal or family mission statement. You can choose to fund your grand passions, purposes and missions or you can forfeit your wealth to politicians and bureaucrats who deem themselves to be wiser than you.

Creating Your Plan

The primary definition of estate planning in this country is, “When you’re dead, how are you going to divide up your stuff?” But that’s only Level 1 of estate planning. Level 2 is, “You have an estate while you’re alive, so what can you do to make the most of your cash flow and wealth while you’re alive to benefit you and your family now and during the course of your lifetime? And then after you pass away, what are you going to do to distribute your cash flow and wealth effectively, and to whom, where and when will it be distributed?” That’s a better approach than Level 1, but there’s a higher level, a Level 3, where I think the game really ought to be played. Level 3 is far more enlightened and rewarding than “estate planning.” Level 3 has far more substance to it, and that is, “What’s your 100-year plan? What are you going to be doing while you’re alive to fulfill your 100-year plan and how is that going to be carried on after your passing?”

Basically, the 100-year plan breaks down into two parts:

For example, if your estimated life expectancy were another 25 years, your plan would break down as follows:

It’s not just an issue of taking care of yourself or distributing money to your heirs; it goes way beyond that to creating a legacy after you pass on. If you’re 60 years old when I meet you, you may think a 100-year plan doesn’t make sense for you, but it really does. If you can get your heirs to accept this 100-year philosophy of life, then how much more effective are you going to be and how much more effective are they going to be? The big picture questions raise us out of the mundane, rudimentary existence which most people lead, the day-to-day, survival existence. How do you define success? How do you really achieve fulfillment? May I suggest that one well proven way to find happiness and fulfillment is by being actively engaged with other people or viable, worthwhile causes, purposes and missions that give you energy and fill you with a passion for life?

When people begin to think in terms of their 100-year plan, there is often a profound impact on their lives and the lives of countless others because their plans become bigger than just themselves or bigger than just them and their families. When you engage in causes and activities that stretch you beyond your desire for comfort and safety, you begin to experience self transcendence.

Think of these words, recorded in Four Minute Essays, Volume IV, by Dr. Frank Crane:

Basically, the 100-year plan breaks down into two parts:

- The balance of your lifetime

- After you're dead

For example, if your estimated life expectancy were another 25 years, your plan would break down as follows:

- 25-year lifetime legacy (what you want to do with your life and how you will enjoy your cash flow and wealth while you’re alive)

- 75-year family and community legacy (what you want your cash flow and wealth to accomplish after you’ve passed away)

It’s not just an issue of taking care of yourself or distributing money to your heirs; it goes way beyond that to creating a legacy after you pass on. If you’re 60 years old when I meet you, you may think a 100-year plan doesn’t make sense for you, but it really does. If you can get your heirs to accept this 100-year philosophy of life, then how much more effective are you going to be and how much more effective are they going to be? The big picture questions raise us out of the mundane, rudimentary existence which most people lead, the day-to-day, survival existence. How do you define success? How do you really achieve fulfillment? May I suggest that one well proven way to find happiness and fulfillment is by being actively engaged with other people or viable, worthwhile causes, purposes and missions that give you energy and fill you with a passion for life?

When people begin to think in terms of their 100-year plan, there is often a profound impact on their lives and the lives of countless others because their plans become bigger than just themselves or bigger than just them and their families. When you engage in causes and activities that stretch you beyond your desire for comfort and safety, you begin to experience self transcendence.

Think of these words, recorded in Four Minute Essays, Volume IV, by Dr. Frank Crane:

|

Make no little plans.

They have no magic to stir men’s blood and probably themselves will not be realized. Make big plans. Aim high in hope and work, remembering that a noble, logical diagram once recorded will never die, but |

long after we are gone

will be a living thing asserting itself, with ever growing insistency. Remember that our sons and grandsons are going to do things that would stagger us. Let your watchword be order and your beacon, beauty. D. Burnham |

The Lifetime Legacy

The first part of the 100-year plan, the “lifetime legacy,” should focus on what your ideal life and perfect calendar(s) would be as well as your personal and family goals and aspirations during your lifetime. Your finances should be arranged (perhaps changed) into alignment with your ideal life, perfect calendar(s), personal and family goals and mission. This will empower you to enjoy full realization of your goals and the life you really want to live. In order to take full advantage of this type of plan, we must dare to dream bigger and more daring dreams. We will almost assuredly require third-party assistance for this because, as individuals, we are highly unlikely to see or comprehend all that’s possible for us. We must create a Macro Strategic Plan® in order to replace the customary thinking, status quo, ambiguity, chaos or conditions which bind us where we are and separate us from that more empowered ideal life and perfect calendar.

It would be wonderful if we had a financial advisor who also understood respected and applied human nature, psychology, spirituality and emotion into our financial plans. As you probably know, the old neuroscience taught us that the two hemispheres of our brain are different. The right hemisphere is more creative and emotional, while the left hemisphere is more analytical and logical. The latest neuroscience proves that our brains are more complex than that. The real magic occurs when we get our entire brain to work simultaneously when setting and achieving goals. The overly simplified way of saying this is; We need to use the right side of our brains to dream up and imagine of all the possibilities available to us, and then use the left side of our brains to help us rationally form a plan and implement the micro details necessary to accomplish those goals. No matter who you are, you will benefit greatly if you and your advisors use a whole-brain rather than a half-brained or fractional brain approach when imagining, designing and creating your ideal life and perfect calendar(s). Sometimes you may have to look beyond your own or your existing advisors imaginations and capabilities if you really do want to enjoy a better, more fulfilling and joyful life. To some extent, we are all limited by our own imaginations, life experiences, preferences, traditions, cultures and beliefs. But what most people fail to realize is this; to a very large extent, we are also limited by the level of awareness, imagination, intelligence and wisdom of our chosen advisors. These can include parents, siblings, spouses, professors, authors, news journalists, colleagues as well as CPAs, lawyers, doctors, bankers, financial advisors, etc.

It would be wonderful if we had a financial advisor who also understood respected and applied human nature, psychology, spirituality and emotion into our financial plans. As you probably know, the old neuroscience taught us that the two hemispheres of our brain are different. The right hemisphere is more creative and emotional, while the left hemisphere is more analytical and logical. The latest neuroscience proves that our brains are more complex than that. The real magic occurs when we get our entire brain to work simultaneously when setting and achieving goals. The overly simplified way of saying this is; We need to use the right side of our brains to dream up and imagine of all the possibilities available to us, and then use the left side of our brains to help us rationally form a plan and implement the micro details necessary to accomplish those goals. No matter who you are, you will benefit greatly if you and your advisors use a whole-brain rather than a half-brained or fractional brain approach when imagining, designing and creating your ideal life and perfect calendar(s). Sometimes you may have to look beyond your own or your existing advisors imaginations and capabilities if you really do want to enjoy a better, more fulfilling and joyful life. To some extent, we are all limited by our own imaginations, life experiences, preferences, traditions, cultures and beliefs. But what most people fail to realize is this; to a very large extent, we are also limited by the level of awareness, imagination, intelligence and wisdom of our chosen advisors. These can include parents, siblings, spouses, professors, authors, news journalists, colleagues as well as CPAs, lawyers, doctors, bankers, financial advisors, etc.

The Family/Community Legacy

The second part of the 100-year plan, the “family/community legacy,” deals with what happens after you’ve died. What can you do with your cash flow and wealth to benefit your family and the community? This part of the plan deals with issues, people and causes that are nearest and dearest to your heart (often referred to as right-brain issues) and the most effective means (strategies, tactics and tools) to address and benefit those people and causes (left-brain issues).

A properly executed 100-year plan is a balance of left-brain and right-brain issues. Balanced Whole Brain thinking is critical to success. If all of this seems complicated and difficult, you’re not alone. Anything great or worthwhile tends to be difficult and it usually requires several dedicated capable people to get the desired results. If this were not true, everyone would be great and happy. True happiness requires an uncommon level of thought and boldness of heart. Happiness also requires a well thought out list of goals and an accompanying strategic plan to carry them out. Sometimes to be happy, we must let go of beliefs, habits, urges, ideology, traditions, immaturity, ego, possessions, pain, grudges, bitterness or people which separate us from the happiness and fulfillment we desire. Perhaps this is part of why happiness can seem so rare or temporary. It seems to me that many people who claim they want more happiness just are not sufficiently willing to let go of whatever is separating them from happiness.

At times, this long-term Macro Strategic Planning® process might seem a bit overwhelming, complicated or difficult. Perhaps we can take some consolation in this thought: You can’t expect to deal with all the macro issues and tie up all the micro issues or loose ends overnight. Instead of becoming overwhelmed by complication, fear, doubt, analysis paralysis, etc, you can establish a timeline for your macro and micro planning and execution. Your timeline should set written realistic goals for:

A properly executed 100-year plan is a balance of left-brain and right-brain issues. Balanced Whole Brain thinking is critical to success. If all of this seems complicated and difficult, you’re not alone. Anything great or worthwhile tends to be difficult and it usually requires several dedicated capable people to get the desired results. If this were not true, everyone would be great and happy. True happiness requires an uncommon level of thought and boldness of heart. Happiness also requires a well thought out list of goals and an accompanying strategic plan to carry them out. Sometimes to be happy, we must let go of beliefs, habits, urges, ideology, traditions, immaturity, ego, possessions, pain, grudges, bitterness or people which separate us from the happiness and fulfillment we desire. Perhaps this is part of why happiness can seem so rare or temporary. It seems to me that many people who claim they want more happiness just are not sufficiently willing to let go of whatever is separating them from happiness.

At times, this long-term Macro Strategic Planning® process might seem a bit overwhelming, complicated or difficult. Perhaps we can take some consolation in this thought: You can’t expect to deal with all the macro issues and tie up all the micro issues or loose ends overnight. Instead of becoming overwhelmed by complication, fear, doubt, analysis paralysis, etc, you can establish a timeline for your macro and micro planning and execution. Your timeline should set written realistic goals for:

- Gathering and assimilating information on goal setting.

- Establishing written, specific, articulate goals.

- Developing your perfect calendar.

- Drafting macro and micro strategic plans to carry out those goals.

- Implementing the planning.

- Systematically reviewing the goals and execution timeline.

- Systematically adjusting the vision, goals, strategies, tactics, tools, timing, personnel and budget(s).

- Being constantly vigilant about the people involved and being certain that everyone (including you) is acting responsibly and being held accountable is crucial to your success.

With a proper tough and confident attitude, more knowledge, constant vigilance, objective help and an adequate balance of WHOLE BRAIN thought, we can all become more effective, successful and happy. What’s more, with a 100-year plan we can be instrumental in the success of many others. It is a necessary part of the fulfillment of human existence to be engaged in something bigger than ourselves. A 100-year plan makes all of this possible, but only if we have the strength of mind, character and competency to put it into action.

If the idea of a 100-year plan is interesting, you’re going to really find 500- and 1,000-year thinking and planning to be intriguing. You are likely to encounter skeptics and cynics who doubt the merit of such long term planning. They often argue that the transient nature of financial markets, politics, tax law, etc invalidates any planning beyond a few years. Many professionals have actually been conditioned to think that way and they don’t know how to think in bigger and longer terms. That kind of thinking is a demonstration of limited fractional brain awareness. Such a condition is usually overcome by any person who really wants to be stretched and empowered into new levels of awareness and effectiveness. That stretching begins by forcing oneself out of fractional brain limited focus on that which is transient and expanding the focus to include that which is capable of enduring for 1,000 years or longer. However, for such growth, you and your advisors must be sufficiently willing to admit existing limitations and to grow beyond them. Willing students and seekers enjoy profound advantages over skeptics and cynics who are resistant to new awareness.

For more than twenty-five years, we have helped our clients and their trusted advisors expand their imaginations, explore new possibilities and accomplish previously unavailable results. When you alter and expand what you think about, you will come to see new ideas and possibilities that used to be invisible to you. That which once seemed impossible becomes possible and then available. We invite you to expand your vision and possibilities and take your life, business, finances and well being to a WHOLE new level of effectiveness.

To arrange your completely confidential strategy session, call us at 805-527-7516 or email us at info@macrostrategicdesign.com.

If the idea of a 100-year plan is interesting, you’re going to really find 500- and 1,000-year thinking and planning to be intriguing. You are likely to encounter skeptics and cynics who doubt the merit of such long term planning. They often argue that the transient nature of financial markets, politics, tax law, etc invalidates any planning beyond a few years. Many professionals have actually been conditioned to think that way and they don’t know how to think in bigger and longer terms. That kind of thinking is a demonstration of limited fractional brain awareness. Such a condition is usually overcome by any person who really wants to be stretched and empowered into new levels of awareness and effectiveness. That stretching begins by forcing oneself out of fractional brain limited focus on that which is transient and expanding the focus to include that which is capable of enduring for 1,000 years or longer. However, for such growth, you and your advisors must be sufficiently willing to admit existing limitations and to grow beyond them. Willing students and seekers enjoy profound advantages over skeptics and cynics who are resistant to new awareness.

For more than twenty-five years, we have helped our clients and their trusted advisors expand their imaginations, explore new possibilities and accomplish previously unavailable results. When you alter and expand what you think about, you will come to see new ideas and possibilities that used to be invisible to you. That which once seemed impossible becomes possible and then available. We invite you to expand your vision and possibilities and take your life, business, finances and well being to a WHOLE new level of effectiveness.

To arrange your completely confidential strategy session, call us at 805-527-7516 or email us at info@macrostrategicdesign.com.